MBA7101 Research Methods and Academic Skill Report 2 Sample

Topic: Impact of Digital Payment on Customer Behaviour

Please be aware that the proposal will continue till next semester. I need to collect quantitative data, and this should be focused on customers.

The following structure must be followed to fulfill the requirements for Assignment 2:

Mini Draft Literature Review

• Word Count: 2000 words

• Deadline: December 24, 2024

• Objective: Align with Learning Outcome 4 (LO4) by synthesizing and critically evaluating relevant literature in a complex research area.

Key Requirements:

1. Clarity and Presentation:

• Ensure the report is well-structured and presented clearly.

• Writing should be critical, concise, and coherent throughout.

2. Critical Analysis:

• Provide a detailed critique of the literature, emphasizing strengths and weaknesses of sources.

• Highlight the relevance and reliability of different studies.

3. Thematic Organization:

• Organize the content in a logical sequence, ensuring smooth transitions between sections.

4. Identification of Gaps:

• Clearly articulate gaps in the existing literature.

• Justify the need for further research in the chosen area.

Assignment Structure:

1. Introduction:

• Provide an overview of the research topic and its significance.

• Outline the purpose and objectives of the literature review.

2. Definitions:

• Define key terms and concepts relevant to the topic to establish clarity.

3. Theories:

• Discuss existing theories underpinning the research area, critically evaluating their applicability and limitations.

4. Conceptual Framework:

• Framework Development: Develop a conceptual model relevant to the research area.

• Relationship Between Concepts: Explain the connections between key concepts within the framework.

5. Research/Knowledge Gap:

• Identify and articulate gaps in the current literature.

• Justify the necessity for further research, referencing how your study can contribute to the field.

6. References:

• Types of Sources:

• Books

• Journal Articles

• Company Websites

• Published Reports

• Government Reports

Minimum Requirements:

• 15-20 sources, including at least:

• Four refereed academic journals

• Five academic books

Additional Notes:

• This literature review serves as a foundation and will be continued in the next semester. Building on this assignment is essential for future progress.

• Writing Quality: Maintain a professional and academic tone, focusing on concise and analytical writing.

• Referencing: Ensure all sources are properly cited using the required referencing style.

Please review the structure and requirements outlined above and start drafting the assignment accordingly. Feel free to reach out with any questions or clarifications needed!

Solution

Introduction

The topic of the present research is analysing the impact of digital payment systems on consumer behaviour parameters within operations of Fintech Industry in Saudi Arabia. It is highly significant in today’s time as it sheds core attention to changing the Fintech ecosystem, with 85% of consumers showing interest in digital payment platforms for wider services. The Saudi Arabia digital payment vision in 2030 focuses on eliminating cash dependency for building a cashless society, in growing varied e-commerce platforms for better advanced services. The purpose and objectives of the literature review for university assignment help are to analyse the core focus on themes related to the topic to establish clarity, evaluate applicability, and identify limitations. It's important to analyse the proper attention to consumer attitudes for integrating diverse competitive sustainable fintech industry operations.

Definitions

Digital payment: The digital payment systems in the market offer new advantages for faster, safer, and easier, less expensive business. Electronic payment signifies usage of digital channels with QR codes, and instruments such as credit and debit. Saudi Arabia has been promoting digital payments as part of its financial sector Vision 2030 to create change in the economy (Central Banking News Desk, 2024). Saudi Arabia has around 150 fintech companies and is growing widely with new initiatives like Fintech Saudi driving innovation, SAMA sandbox under Vision 2030. Digital wallets include Apple Pay and Google Pay, user loading money into virtual wallet systems along with STC Pay within growing demands. Crypto currencies includes Bitcoin, Litecoin and payment gateways are also there, facilitating new transactions between merchants and consumers in Saudi Arabia offering new payment with high checkout options.

Fintech industry: Saudia Arabia's Fintech industry is growing with expectations to reach $63.9 billion in 2024, driven by new innovation in strong government with tech-savvy new strategic initiatives (Central Banking News Desk, 2024). Digital payments have reached around 70% of retail transactions, up from 62% in 2022. Transactions by digital means have shaped new national payment systems that grew by 24% to a further 10.8 billion payments. Fintech industry payment options have a highly varied scope, bringing new consumer opportunities and larger diverse sustainable constant change targets. Saudi Arabia Fintech ecosystem is huge and highly competitive, with expectations to grow from 63 billion In recent 2024 to benchmark of 87.14 billon by 2029. The CAGR is growing than 6% during forecast period. Some major examples growing essentially are online banking, crowd funding and peer to peer lending along with new block chain initiatives commercially on successive new platforms.

Theories

Assessing Factors Impacting Customer Adoption of Digital payment methods

As stated by Rawat (2024) there are various factors which impact customer adoption of digital payment methods in Fintech industry operations. Mobile payment adoption comes with multiple factors affecting preferences among customers for digital banking, and new perceived dimensions. It's important to check perceived ease of usage, usefulness and trust in technology for customers to adopt digital payment. The author's research has signified the core importance of assessing factors impacting customer adoption of diverse digital payment methods, within the fintech sector growth targets of Saudi Arabia.

Saudi Arabia's fintech market is growing towards productive usage of advanced technology infrastructure, new accessibility for best fast services and 5G networks for increasing demands like insurance, asset management (Saudi Arabia’s Ambition towards a Cashless Kingdom by 2030, 2020). Buy now, Pay later, crypto and block chain, contactless payments are some major new innovative platforms used by consumers. This signifies an increase in customer demands and adoption of new digital payment methods diverse factors, and larger successive pace in Fintech industry. It also analysed changing market parameters and constant aspect, for changing parameters in new digital payment methods.

Research by Hasan et al., (2024) signifies us Technology acceptance model signifies consumers accept and use new technologies including advanced online payment systems. There are cultural and economic factors in correlation to TAM theory are very crucial, some economic aspects are Saudi Arabia vision for cashless economy and digital payment acceptance along with subsidies. Also economy is highly competitive towards broader payment accessibility, economic inclusivity focused on usefulness and higher cost effective solutions. In cultural factors consumers spending and willingness for technologies for cashless payments, QR code systems are growing in Saudi Arabia

Perceived usefulness focuses on government endorsed platforms and enhancing digital payments convenience for consumers, also on economic inclusivity and vitally focusing on driving adopting various new technologies. Digital infrastructure, user friendly designs reduces barriers for adoption in digital payment technologies within Saudi Arabia.

TAM constructs signify external variables, perceived usefulness and new behavioural intention-based aspects efficiently explored It highly correlates with the usage of digital payment methods, consumers perceive risk, trust and security, and privacy before acceptance. Social norms also play a significant role in shaping electronic payment behaviour diversely and modern technologies such as social networks, affect consumer preferences. Recent data has showed informative aspects, regarding changing market pace and competitive change standards towards cashless fintech market (Saudi Arabia’s Ambition Towards a Cashless Kingdom by 2030, 2020). Therefore, research has specified important factors investigating user acceptance of mobile payments among consumers.

As per the views of Febrianto et al., (2023) study shows trust in perceived risk and security, satisfaction has a profound impact on consumers' perception towards digital payment methods. It affirms various factors for surveying new demands in digital payment goals, and increased importance within digitalized mechanisms in business landscape. The author signifies the important usage of technological innovation within the rise of customer adoption of new digital payment methods in Fintech industry. Present study signifies more accurate analysis on changing demands of consumers for adoption of digital payments, and new trends within the Fintech business. The new analysis also personifies authors views and specific changed economic patterns, due to consumer demands and new Fintech industry domains specifically.

As stated by Norbu et al., (2024) blockchain technology adoption in digital payments mechanisms holds huge importance for various factors such as privacy, adoption of new transparent decisions are there. The most important factors identified in the paper are the unified theory of acceptance, wider use of the technology model including usage of performance expectancy, and new demands for digital payments. Incorporating new models with viable approaches tackles obstacles and ensures integration of advanced systems, bringing wider scale constant changes in the Fintech business (Thunes, 2024). The integration of user perspective research within dimensions of blockchain adoption in digital payment systems is sufficient, with attention on productive users' perspectives for new potentialities. The review has shed light on factors of trust, and new acceptance of technology change related to potential blockchain technology integration.

However, as stated by BCI (2024), some risk factors in the adoption of customers’ adoption of new digital payment methods are there which impact the growth of the Fintech industry. Some major risks and challenges customers feel are security, and privacy risks of digital transactions, technical issues and transaction fees. It can be also stated that these have a profound impact on customers’ choices and overall preferences for choosing digital payment methods.

Risks associated with Digital Payments Affecting Consumers

As stated by Idayani et al., (2024) some major risks of adopting new online payment systems impacting consumer behaviour in the fintech industry are the risk of fraud, and technical issues related to cyber security. The author of present research has stated core importance to these aspects based on changing preferences, risks and challenges in digital payment impacting consumer behaviour standards in fintech. Identity theft, loss of cards and online data unfamiliarity with technology are some major risks associated with changing consumer behaviour. This research provides authentic data based on facts on how cyber-risk affects, usage of fintech business signifies better development.

As per the views of Chatterjee et al., (2024) some new informative in-depth analyses have been done on exploring credit fraud risk factors, a current fraud detection techniques. The author has stated attention to the use of digital twin technologies, for overcoming identified risks among fintech risks. Blockchain enables new federation and usage of models, with sensitive data improved fraud detection. Surely decentralized characteristics of blockchain ensure a transparent, secure approach to preventing fraud in financial business goals.

As per the views of Alnemer (2022), fintech encompasses new innovative technical aspects to improve new technical solutions in business, have wider determined role with changing consumer demands. In order to remain innovative and consumer-focused, the financial services and banking sector in the fintech business have new scope to expand on digital advertising, digital insurance, and crowd funding goals. The emergence of fintech services in recent times has been substantially growing within new business parameters, by providing inventive solutions for improving accessibility transformation. Peer-to-peer lending platforms has also shaped new sustainable financial practices and stimulated new economic growth goals. The paper has also analysed new factors for combatting risks and working on wider scale changes innovatively as per growing digital payments affecting consumers’ demands specifically.

As stated by Kumar (2024), technological developments have created a competitive environment, and businesses adapting to new changes and trends related to digital payment systems. Consumers in developing regions face major obstacles in developing systems, challenges such as privacy concerns, and fear of data breaches are there in embracing online payment mechanisms. The paper explains the diffusion of innovations theory offering a perspective on the adoption of new methods, focused on the diffusion process helping businesses and policymakers design new strategies among consumer segments. Authors views analysed in paper signify new technological innovation, specific new initiatives taken up in digital payments.

As opined by Ramayanti et al., (2024) emergence of new innovations in the fintech business has created shift in digital payment systems focusing on new one click payment mechanisms. There is definitely growth seen in digital payments as successful innovation, with components of save time efforts and a rise in online techniques for transactions. In 2020, 2.4 billion people used digital banking with the expectation of 3.6 billion in four years based on changing expansion of Internet transactions significantly. The article has informatively explained the new scope of fintech business goals, dynamic business change which is overcoming risks associated for customers. Major innovation and new trends are shaping in Fintech industry for curbing the risks faced by consumers, lowering the challenges for consumers specifically. It definitely brings new market changes expand, higher scope among consumers to gain confidence for using online payment systems digitally and lead competent values.

Saudi Arabia fintech industry surely has a high competitive work scope, to bring on the best data technologies for curbing down risks associated with digital payment systems (Thunes, 2024). Therefore, the review has been authentic regarding risks faced by consumers for adopting digital payment systems in the fintech industry.

As stated by Ameerbakhsh et al., (2021) application of user-centred designs in payment systems applies UCD principles for new payment systems tailoring new designs and functionality. It signifies user centered design systems in payment offer several benefits, curbing down risks in online data management among consumers. Improved user satisfaction and trust within a user-centric approach fosters positive emotions, and a new trust in payment systems which is significant for user retention in fintech sector. This signifies new adoption of user-centred design principles for developing digital pay mechanisms, as per changing Saudi Arabia's diverse fintech business goals.

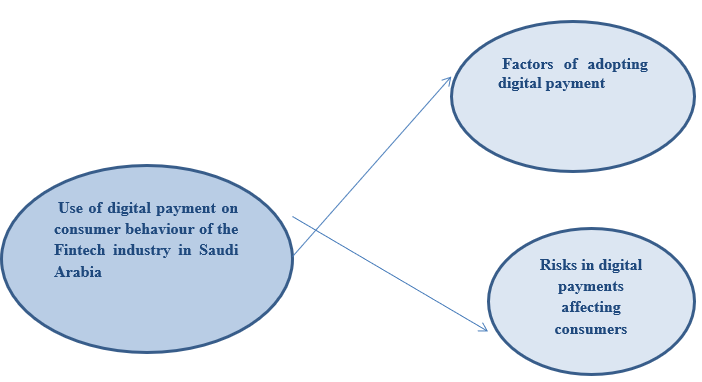

Conceptual Framework

The conceptual framework has reviewed focus on themes and objective of research, various parameters and wider scale dimensions in research. It has also reviewed core attention on latest parameters in use of digital payment on consumer behaviour in Fintech industry of Saudi Arabia. Pictorial representations further add on creative informative aspect on themes analysed and research topic. Conceptual framework focuses on two objectives discussed in literature review study: factors of adopting digital payment and risks in digital payments affecting consumers.

Research/knowledge Gap

The literature review on present topic has stated attention on analysing impact of using digital system of payments among consumer behaviour, within growing Fintech industry operations in Saudi Arabia. Its limited to analysing the impact of digital payments in Fintech operations in only Saudi Arabia only limits the authenticity and new facts related to changing mechanisms. The study is also limited to finding new facts regarding changing other domains of the Fintech industry in the market scenario. The knowledge gap is there at present as it only researches about impact of digital payments on consumer behaviour; many other factors are also there impacting demands among consumer behaviour standards specifically. Literature lacks depth within areas of role of emerging fintech technologies beyond digital payments, creating wider consumers awareness among new financial entrants. There are also new rapid advances in digital technologies are shaping financial landscapes competently within Saudi Arabia fintech ecosystem.

Further new research standards need to be evolved for reviewing of wider dimensions of fintech industry operations within Saudi Arabia. Various new specific domains are coming up in fintech standards, new technologies shaping online payment systems among consumers specifically. This signifies there is a knowledge gap in present literature findings, not in-depth based on the topic. New research in this area further will enable readers to gain insightful new insights into changing demands for digital payments among consumer behaviour.

References

Alnemer, H.A., (2022) Determinants of digital banking adoption in the Kingdom of Saudi Arabia: A technology acceptance model approach. Digital Business, 2(2), p.100037. https://www.sciencedirect.com/science/article/pii/S2666954422000175

Ameerbakhsh, O.Z., Alfadli, I.M. and Ghabban, F.M., (2021) Factors affecting Saudi consumers’ acceptance towards the use of electronic payment. Design Engineering, 5(2), pp.124-136. https://www.researchgate.net/profile/Drfahad-

Ghabban/publication/352519272_Factors_Affecting_Saudi_Consumers'_Acceptance_Towards_the_Use_of_

Electronic_Payment/links/60efa3c90859317dbde2e10d/Factors-Affecting-Saudi-Consumers-Acceptance-Towards-the-Use-of-Electronic-Payment.pdf

BCI. (2024) Saudi Arabia’s Path to Resilience: The Role of Vision 2030. Available at: https://www.thebci.org/news/saudi-arabia-s-path-to-resilience-the-role-of-vision-2030.html [Accessed 12th November 2024].

Central banking newsdesk (2024) Digital payments in Saudi Arabia rise to 70% of retail transactions Available at: https://www.centralbanking.com/central-banks/payments/7961074/digital-payments-in-saudi-arabia-rise-to-70-of-retail-transactions [Accessed 8th December 2024]

Chatterjee, P., Das, D. & Rawat, D.B., (2024) Digital twin for credit card fraud detection: Opportunities, challenges, and fraud detection advancements. Future Generation Computer Systems https://doi.org/10.1016/j.future.2024.04.057

Febrianto, A., Siga, E.C.A.R., Kristin, D.M & Pratama, M.R.K., (2023), November. Digital Payment Adoption Research of SMEs in Emerging Countries: A Systematic Literature Review. In 2023 International Conference on Informatics, Multimedia, Cyber and Informations System (ICIMCIS) (pp. 432-439). IEEE. 10.1109/ICIMCIS60089.2023.10349051

Hasan, A., Alenazy, A.A., Habib, S. and Husain, S., (2024) Examining the drivers and barriers to adoption of e-government services in Saudi Arabia. Journal of Innovative Digital Transformation. https://www.emerald.com/insight/content/doi/10.1108/JIDT-09-2023-0019/full/pdf

Idayani, R.W., Nadlifatin, R., Subriadi, A.P.& Gumasing, M.J.J., (2024). A Comprehensive Review on How Cyber Risk Will Affect the Use of Fintech. Procedia Computer Science, 234, pp.1356-1363 https://doi.org/10.1016/j.procs.2024.03.134

KUMAR, V.V., (2024) Mobile Commerce and the Rise of M-payment Systems: A Study of Emerging Trends and Consumer Adoption. https://www.ijesat.com/ijesat/files/V24I1030_1728568164.pdf

Norbu, T., Park, J.Y., Wong, K.W & Cui, H., (2024). Factors affecting trust and acceptance for blockchain adoption in digital payment systems: A systematic review. Future Internet, 16(3), p.106. https://doi.org/10.3390/fi16030106

Ramayanti, R., Rachmawati, N.A., Azhar, Z. & Azman, N.H.N., (2024). Exploring intention and actual use in digital payments: A systematic review and roadmap for future research. Computers in Human Behavior Reports, 13, p.100348. https://doi.org/10.1016/j.chbr.2023.100348

Rawat, P., Muthulakshmi, R., Josyula, H. P., Kataria, A., & Landge, S. R. (2024). Consumer Perception And Adoption Of Digital Payment Methods: A Study On Trust And Security Concerns. Educational Administration: Theory and Practice, 30(4), 6022-6029. https://doi.org/10.53555/kuey.v30i4.2334

Saudi Arabia’s Ambition Towards a Cashless Kingdom by 2030 (2020) Available at: https://ycp.com/about/corporate-update/saudi-arabias-ambition-towards-a-cashless-kingdom-by-2030 [Accessed 6th Dcember 2024]

Thunes (2024) Saudi Arabia, the Middle East’s next fintech oasis Available at: https://www.thunes.com/insights/trends/saudi-arabia-the-middle-easts-next-fintech-oasis/ [Accessed 6th Dcember 2024]

Fill the form to continue reading

Would you like to schedule a callback?

Send us a message and we will get back to you

Highlights

Earn While You Learn With Us

Confidentiality Agreement

Money Back Guarantee

Live Expert Sessions

550+ Ph.D Experts

21 Step Quality Check

100% Quality

24*7 Live Help

On Time Delivery

Plagiarism-Free

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU