LAW6001 Taxation Law Case Study Sample

Task Summary

In response to the issues raised in the case study provided, research and develop a 2000-word tax advice that addresses (a) assessable income (b) allowable deductions (c) calculations of income/deductions and (d) your conclusions and recommendations.

Please refer to the Task Instructions for details on how to complete this task.

Context

This assessment assesses your research skills, your ability to synthesise an original piece of work to specific content requirements and your ability to produce a comprehensible piece of advice which addressing the client’s needs. It also assesses your written communication skills. The ability to deliver to a brief is an essential skill in the workplace. Clients may well approach advisors seeking a combination of specific information needs and advice on the tax implications of a particular arrangement in the Australian tax jurisdiction. It is therefore important to be able to identify all the issues presented by an arrangement and to think about the potential consequences of different approaches to addressing the client’s needs.

Task Instructions

• Your case study needs to identify and discuss the tax implications of the various issues

raised.

• A report (word document, approx. 2,000 words) must be submitted for the calculations of the assessable income; allowable deductions and taxable income of the taxpayer including identifying and discussing them. E.g., how the amounts of income & deductions have been derived. If any receipts and payments are not assessable or deductible, the reasoning for non-inclusion of these in assessable income or deductions as per relevant legislation or cases.

• Critically analyse the following case study.

With respect to each task:

• Review relevant case law and legislation (ITAA1936, ITAA1997)

• Apply the law to the facts of the case study

• Reach a conclusion/ give practical advice to your client.

• You will be assessed in accordance with the Assessment Rubric.

• This case study must be presented as an individual effort. The case study requires individual research. It is expected the student will survey the relevant literature, including decided cases, and select appropriate additional resources.

• Your case study is not just a list of answers. Your reasons for your conclusions and recommendations must be based on your research into the relevant cases and legislation.

• The format of the report should be a business report and using APA referencing style.

Solution

Answer-1

Issue

In the above case scenario the concerning issue is to provide advice as per relevant legislations and cases on the deductibility of the expenses for repairs and improvement from the assessable income of the Ken.

Rules and Regulations

Deductions could reduce the income of an individual from certain losses and outgoings incurred in the process of production of assessable income. For Assignment Help, As per the D 8 of Income Tax Assessment Act 1997, the deductions are categorized in two sub parts that are general deductions and specific deductions. General deductions are mentioned in the division 8.1 of the ITAA 1997, which consists of those expenses that are incurred in the production of assessable income or for the purpose of carrying a business for gaining assessable income as per section 8.1(1). Further, in the section8.1(2), it is stated that,expensesof capital nature, expense made for domestic and private use or incurred in producing non- assessable income would not be deductible. In the case of Charlie’s Moore & CO Pty ltd v FCT, the losses were held to be deductible as the loss was incurred in the process of running the business (Burgess, 2018).

As per division 8.5 in ITAA 1997, specific deductions are those deductions which could reduce the income of an individual as per some specific sections apart from the general deduction of the legislative authority. Further, in subsection division 25in ITAA 1997 expenditures which are incurred for repair to premises could be deducted from the assessable income of taxpayer. In case if the taxpayer has incurred expense for repair on the depreciating asset which is solely used for producing the assessable income could be deducted from assessable profit (division 25-10(1)). Taxation ruling 97/23 was specifically released for the analysis of tax deductibility of expenses incurred by taxpayer for repairs (Borkes, 2018). Repair means remedying defects in damages, deterioration of property which is repaired and contemplate the existence of such property. Further the work done for the purpose of improvement or addition in the property is not included in repairs and would not be deductible as per section 25-10.

Repair v Improvement

Repair occurs when there is restoration of efficiency in function is done but improvement results in addition of the advantages of that particular asset (Gough, 2017). As per W Thomas minor improvement which enhances the efficiency could be deductible as all the repairs improve the condition is being held. Further in context to this in the case law of Morcom v Campbell-Johnson replacement with the modern equivalent equipment is deemed to be repair.

Repair v Reconstruction (entirety and subsidiary parts)

Capital items which are specifically identifiable or not necessarily whole but substantially the whole of the property refer as entirety. In the legal case of Lindsay v FCT a part of the premises that is slipway was constructed by the taxpayer on which repairing of ship business was carried out (Todd, and Fiona. 2018). The slipway was held to be an entirety in itself. But the expenditures which went beyond the replacement of subsidiary parts would not be deductible as repairs.

Initial repairs

The initial repairs which are not deductible from the fact that it states the disrepair which is reflected in the assets purchase price or the initial repair which enhances the functional ability of the asset that didn’t possessed when it first came in existence of taxpayer’s ownership. In the case of Law Shipping Company, the deductions were denied by the court and explanation was provided that sate of disrepair was reflected in the ship’s purchase price.

Further the subsection of 25-10(3) states the non deductibility of the capital nature expenses as a repair. For example the expenses which are made for the purpose of reconstruction of entirety of property, replacement or enlargement of profit yield and acquisition of capital asset (Joseph, 2017).

Application

In the given case study Ken acquired a restaurant paying $850,000 for the land and buildings, plant, goodwill and equipment. Such expenses are considered as capital nature and therefore same is not allowed to deduct from assessable profit.

In August 2020, at the initial stage for the purpose of opening the restaurant Ken realized the repairing of electrical system which cost $27,000 to him. As per the above study it could be said that the expenses made by Ken for repairing of electrical system for the purpose of starting the business is considered as capital nature expenditure further it is part of initial repairing which is non- deductible. Hence would not be deductible from his income. Further after opening the restaurant Ken had to replace cracked tiles of the kitchen wall, restoring them, costing $6,400. Since the tiles were replaced and restored it could not be deductible under repairs as per the TR 97/23.

In November 2020 Ken decided to replace all the kitchen cooking equipment which costs $30,000 to him. As all the cooking equipment were replaced hence would not be deductible as repair because the specific deduction for the repairs does not includes the replacement of the equipments in it. At the same time Ken entered into a contract to have the equipment regularly inspected and serviced, the contract fee was $1,500 per year. As contract made was for the purpose of maintaining the equipments which comes under the maintenance cost and they are deducted as per the general deduction 8.1 in ITAA 1997 from the assessable income of the Ken as these expenses incurred from the production of assessable income. Further, to ensure health and safety measures Ken decided to pay pest Control Company $2000 per year which comes under the ordinary expenses of maintenance and are deductible in the year such expenses were made.

In January 2021 replacement of roof along with insulation and ducted air conditioning was decided by ken. The roof replacement cost worth $32,000 and the insulation and air conditioning cost worth of $7,400. Also an additional room cater for more patronage was constructed which cost $26,800. Such costs which incurred for the purpose of replacement of roof and addition of the room and air conditioners could not be deductible as these are capital nature expenditures as pr the ITAA 1997.

Conclusion

From the above application it could be concluded that cost incurred for repairing electrical system, roof replacement, additional room construction would not be deductible as they are capital expenditures. Also replacing kitchen tiles, and kitchen equipment cost would also be non- deductible as they are replaced. Further the cost of contract fee for regular inspection of equipment and pest control fee could be deductible under general deductions.

Answer 2

Issue

In the above case scenario net capital loss or gains is required to be calculated for Maurice for the income year 20/21.

Rules and Regulations

Capital gain taxes (CGT) are those taxes which are paid on the gain from selling asset such as property or any other fixed assets. The net capital losses and gains are reported in income tax return and tax is paid on the capital gains (Mikesell, 2018.). The net capital gains and losses are raised only through CGT events. CGT assets are such as land, shares, goodwill, stock options, property etc.

Further, the assets which are acquired before CGT was started that is 20th September 1985 are exempted from capital gain taxes. Some of the exempted capital assets also includes main residence of taxpayer, motor vehicle which carries load of less than 1 tone and less than 9 passengers (excluding trucks), depreciating assets, PDF shares (other than dividends), REU’s (Registered emission units) (Mangioni, 2019). Also CGT is applicable on the capital gain of personal use assets which are $10000 or more and capital losses on personal asset are ignored which means capital gains could not be reduced by using the capital losses of the personal use assets (List of CGT assets and exemptions, 2021). Personal use assets are such as furniture, boat and electrical goods and other house use items are exempted from capital gain tax if cost of acquisition is less than $10000. If collectibles is acquired for $500 or more and are acquired after 16 December 1995 such as artwork, antiques etc. are exempted from CGT. In addition to this cost base is another element which is used in calculating the capital gains from CGT events.

Additionally there are two methods of calculating capital gain taxes that are discounted method and indexation method (Minas, and Brett 2020).

Discounted Method

Under this discount capital gains are reduced by discount percentage. Requirements for this method:

• Taxpayer must be Australian resident.

• The asset is owned for at least 12months before the CGT event takes place (CGT discount, 2021).

If the asset is owned for 12 months or more-

• Individuals and trusts = 50%

• Complying superannuation entities = 33?% (section 115-100)

• No discounts for companies.

Further before application of this method capital losses from the other assets are reduced from the capital gains. If the taxpayer is entitled for the discounts he could reduce the reaming capital gain by 50% and report it in the income tax return.

Indexation Method

If the assesse purchased assets prior to 21st September 1999, then they are eligible to index the cost base of assets. To calculate from this method first identify capital costs, then identify CPI for the quarter in which cost was incurred then multiply such cost by the indexation factor. Then total eligible indexed and non -indexed cost and at last subtract indexed cost from the capital proceeds (Indexing the cost base, 2012). Capital proceeds are amount received from the selling of CGT assets or any other CGT events.

Applications

In the given case, Maurice has purchased home on 20th Feb 1989 at a price of $140000, however this home has not been used by taxpayer for income generated purpose. It has been assumed that, this was the main residence of Maurice, and therefore not capital gain tax would be charged.

Further, Maurice has purchased shares in FUL Pty Ltd on 10th April 1984 at a price of $15000. Since, assets has been acquired prior to 20th September 1985, therefore capital gain tax provision would not be applicable in this situation.

Further, furniture is also falls under personal use assets but it is acquired at a price more than $10000, therefore CGT would be applicable.Computation of capital gain or loss for furniture is as follows –

.png)

Further, Yacht is also falls under personal use assets but it is purchased at a price more than $10000, therefore CGT would be applicable.Computation of capital gain or loss for yacht is as follows –

.png)

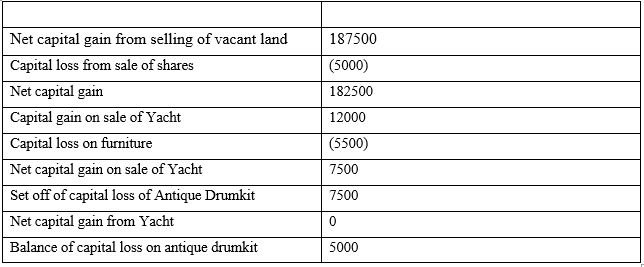

No CGT discount would be applicable on sale of furniture because assets are not hold by Maurice for minimum 12 months.

In the given case, block of vacant land has been acquired as on 20th June 1997 at a price of $100000. The market value of the same as on 15th May 2021 was $475000, but it is sold at a price of $465000, which is less than the market price. By application of above provisions, capital proceeds would be market price of vacant land. Further, in this case, capital gain discount method would be applicable as the assets are hold by Maurice for more than twelve month and he is also Australian resident. Computation of capital gain or loss for vacant land is as follows –

.png)

It has been assumed that, antique drumkit was the personal assets of Maurice, and therefore by application of above provisions, carried forward losses of personal use assets should be ignored and they are not allowed to be set off from gains of other assets. Moreover, carried forward capital loss of $5000 from selling of shares is allowed to be set off from the capital gain of other assets.

Since, sale of Yacht is personal use assets, and therefore capital loss on furniture and carried forwards loss on antique drumkit is allowed to set off from this.

Net capital profit for Maurice for 2020-21 = $182500

Conclusion

As per above application it could be concluded that purchasing of home and shares would not be charged by income tax gain and on furniture and yacht the CGT is applicable. Further, for the computation of vacant land’s capital gain and loss, discounted method is used.

References

Burgess, M. (2018).“International Tax and Estate Planning.” Taxation in Australia 53(1):26–32 https://lesa.on.worldcat.org/v2/search/detail/7794923712?queryString=International%20Tax%20and%20Estate%20Planning&clusterResults=true&groupVariantRecords=false

CGT discount (2021), (online).Retrieved from <https://www.ato.gov.au/Individuals/Capital-gains-tax/CGT-discount/>.

Gough, J. (2017). “Tax Deductions for Rental Property.” The Public Record 40(55):11–11.https://lesa.on.worldcat.org/v2/search/detail/tax%20deductions%20for%20rental%20property

Indexing the cost base (2012), (online) .Retrieved from <https://www.ato.gov.au/Individuals/Capital-gains-tax/Calculating-your-CGT/Cost-base-of-assets/Indexing-the-cost-base/>

List of CGT assets and exemptions, (2021), (online).Retrieved from <https://www.ato.gov.au/Individuals/Capital-gains-tax/List-of-CGT-assets-and-exemptions/>.

Mangioni, V. (2019).“Value Capture Taxation: Alternate Sources of Revenue for Sub-Central Government in Australia.” Journal of Financial Management of Property and Construction 24(2):200–216. https://lesa.on.worldcat.org/v2/search/detail/9054002322?queryString=Value%20Capture%20Taxation%3A%20Alternate%20Sources%20of%20Revenue%20for%20Sub-Central%20Government%20in%20Australia.%E2%80%9D%20&clusterResults=true&groupVariantRecords=false

Mikesell, J.(2018). “Capital Gains Taxation: A Comparative Analysis of Key Issues.” Choice 55(6):767–67. https://lesa.on.worldcat.org/v2/search/detail/7296128580?queryString=Gains%20Taxation%3A%20A%20Comparative%20Analysis%20of%20Key%20Issues&cluster

Results=true&groupVariantRecords=false

Minas, J. and Brett F. (2020). “Australia's 50% Cgt Discount: Policy Oversight?” Australian Tax Forum 35(1):88–107. https://lesa.on.worldcat.org/v2/search/detail/9069174671?queryString=Australia%27s%2050%25%20Cgt%20Discount%3A%20Policy%20Oversight&clusterResults=true

&groupVariantRecords=false

Fill the form to continue reading

Would you like to schedule a callback?

Send us a message and we will get back to you

Highlights

Earn While You Learn With Us

Confidentiality Agreement

Money Back Guarantee

Live Expert Sessions

550+ Ph.D Experts

21 Step Quality Check

100% Quality

24*7 Live Help

On Time Delivery

Plagiarism-Free

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU